Hello From Beautiful Pagosa Country!

It’s a gorgeous morning with bright blue skies and lush, green grass. Finally, we have some good news about bad weather! After enjoying temperatures in the 70s and 80s a month ago, we are now seeing more normal temperatures in the 50’s and 60’s with rain in town and snow in the mountains. That being said, we are still in a severe drought. Our snowpack in the mountains is down to 13% of median for this time of year.

Our local water company, Pagosa Area Water and Sanitation District (PAWSD), has already started stage one drought restrictions. This means you can only water your lawn between 6:00 p.m. and 9:00 a.m. Restaurants will only serve water upon request, and the cost of water is going up.

The drought and associated concerns about wildfires may impact your wallet in other ways. The State of Colorado is mandating new building restrictions to make new homes more fireproof. The state is trying to get out ahead of the situation that other states like California and Florida are facing, where home insurance is becoming increasingly difficult to get. These new regulations are known as the Colorado Wildfire Resiliency Code. Among other things, the new rules require more fire-resistant building materials and techniques for siding, decking, roofing, and doors.

If you’d like more information, you can read about it here:

https://dfpc.colorado.gov/cwrc-what-and-why

Enforcement of the new requirements begins July 1st. There has been a rush of building activity lately as builders try to get their projects in before the new rules start and costs go up. I was in a meeting recently with Randy Betts, who is a building official for Archuleta County. He estimated that the new rules would only cause costs to rise about 2%. But, I have also spoken to several different builders in town, and they think we are looking at a 10% to 15% increase in new construction costs under the new rules.

The increased cost of new construction may affect the value of existing homes as well. If it costs more to build a new house, this can also cause the value of an existing home to rise.

One little piece of good news is that the downtown highway reconstruction project seems to be moving right along. I’ve seen a lot of concrete being poured in recent days. It seems like much of the utility work has been completed. Hopefully, that means we’ll have more of the road work finished by the busy Memorial Day holiday. The project is not due to be completely finished until later this fall.

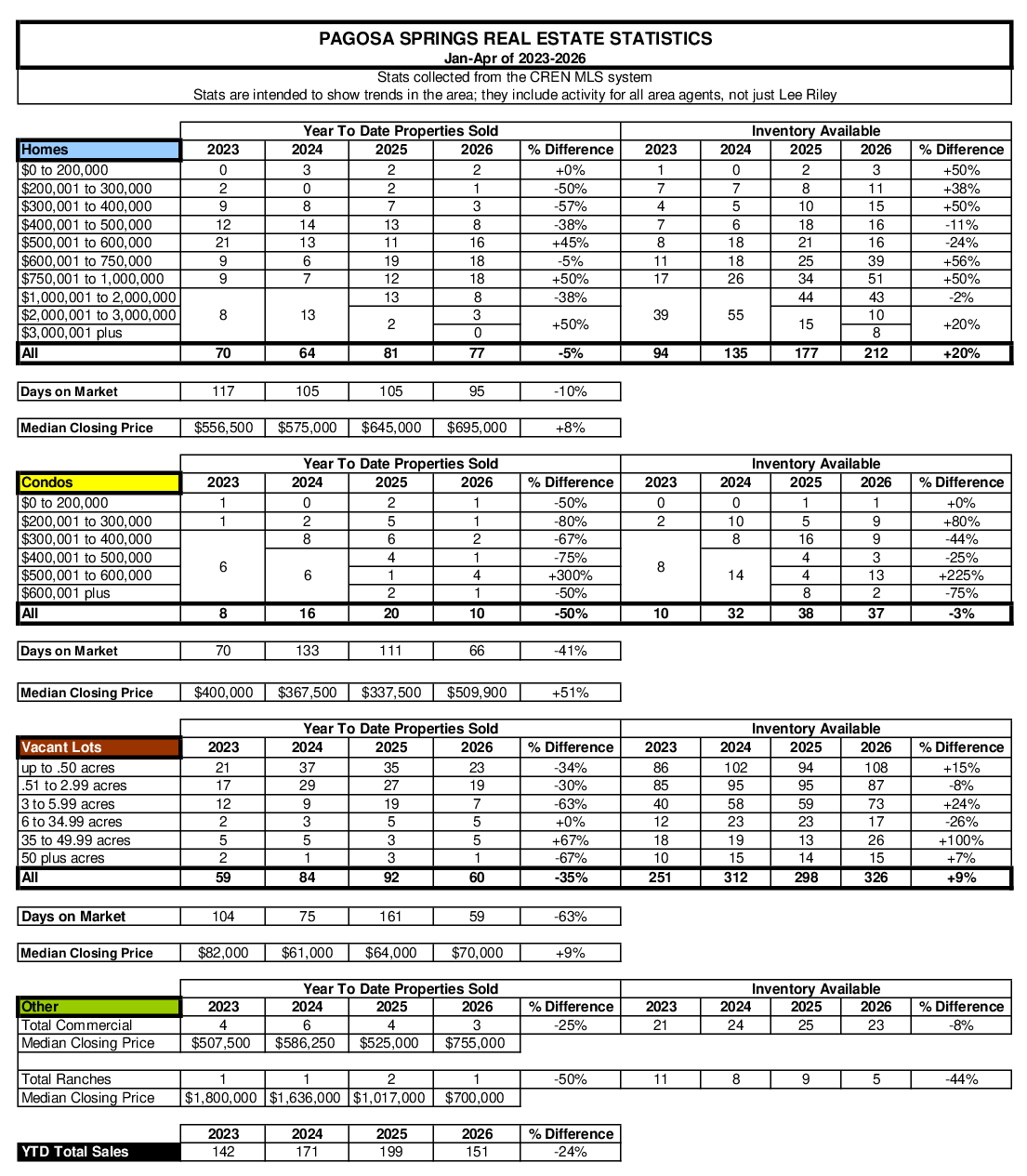

Now for the latest real estate news. The total number of sales year-to-date is down 24% with 151 sales so far this year compared to 199 last year. Home sales are pretty flat. They are only down 5% with 81 this year versus 77 last year. Condo and townhome sales are half of what they were last year. We’ve had 10 sales so far this year compared to 20 last year. Vacant land sales are way down by 35% with 60 this year versus 92 last year.

Inventory is up 20% in the residential category. Condo & townhome sales are down slightly by 3%. Vacant land inventory is up 9%.

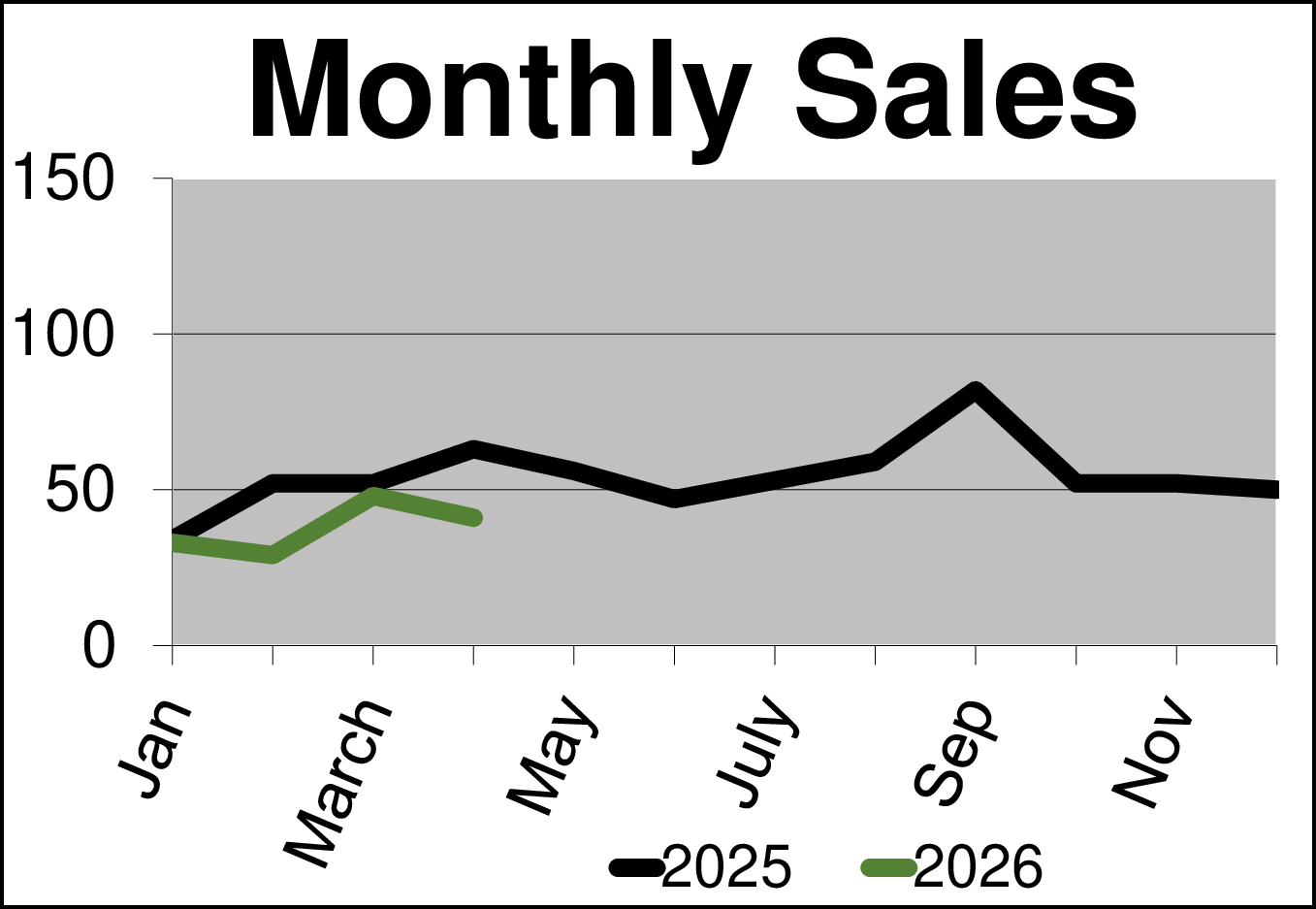

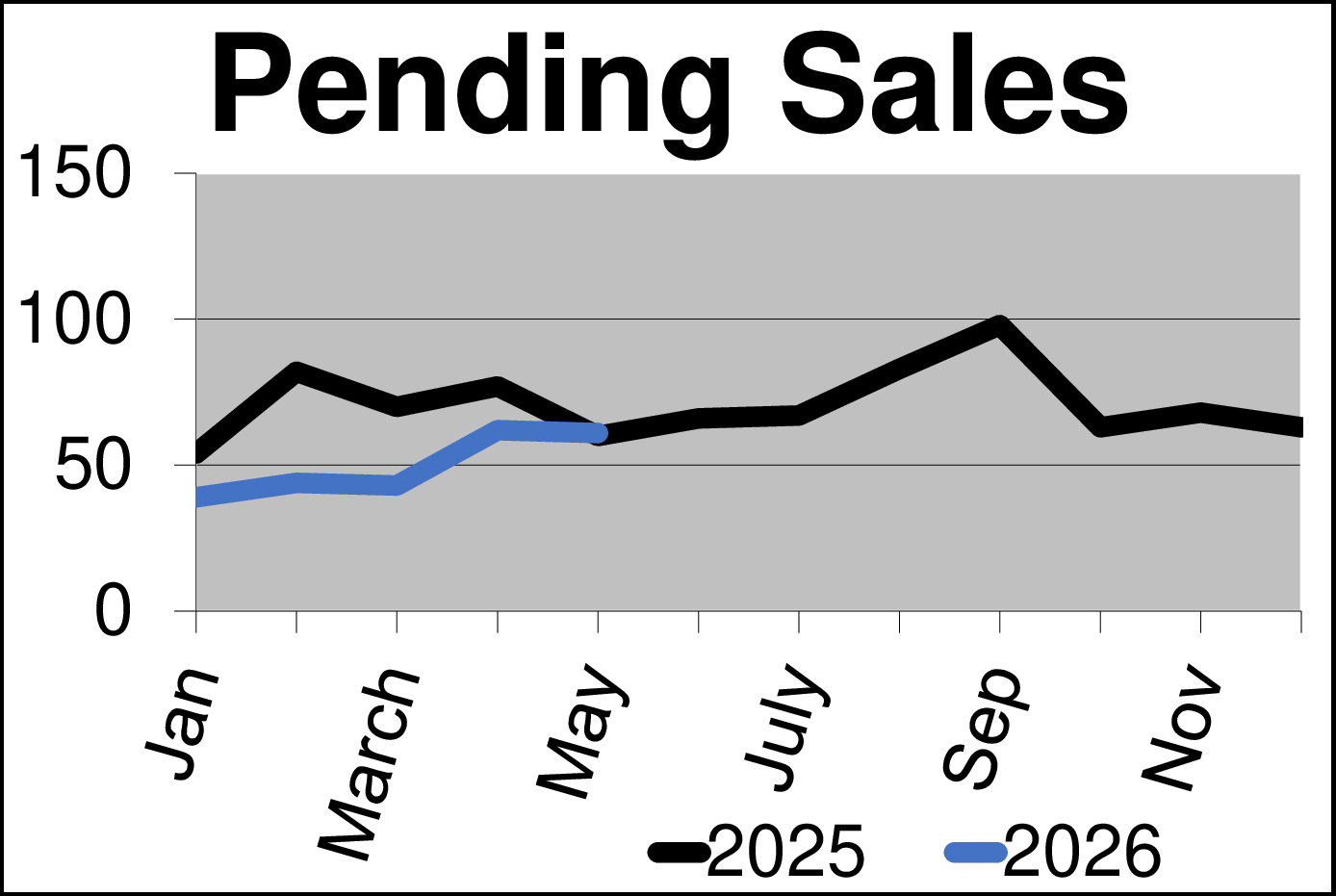

The big story in April is that the total number of sales for the month was way down. We had 41 sales in April compared to 63 last April, which his a 35% decline. Pending sales are flat with 61 today versus 60 a year ago. For more details, check out all the graphs and stats included here.

So, why was April so sluggish? We probably could have predicted a slow month looking at last month’s pending sales, which were way down. We had 62 pending sales last month compared to 77 the previous year. In general, the residential market has been flat. The condo and townhome market is softer to due major increases in HOA fees, which are caused in great part by increases in insurance rates.

Vacant land sales are where we see the greatest decline. The cost of building a new home is part of the story. For example, the cost of hooking up to PAWSD water and sewer has tripled in the last few years. It used to cost $9,000, and now it costs $29,000 to hook up to the water and sewer system. The quality of available home sites is also declining. Most of the cherries have already been picked and built on.

The lower end of the residential spectrum is more heavily influenced by interest rates. Before the war with Iran started, a 30-year fixed-rate mortgage was at 5.99%. It went as high at 6.62% on March 26. Currently, the 30-year fixed rate is at 6.50% and the 15-year is at 6.03%. These rates have jumped due to gas and oil prices skyrocketing. We will have a new Fed chairman coming on board May 15, and I’m sure he would like to cut rates, but the market is suggesting only one rate cut this year if any.

The war is keeping some buyers and sellers on the sidelines waiting to see what happens. If the war ends soon, I think it will jump start the market.

So long for now! Enjoy the spring flowers, think positively, and make today a great day! I want to send out a big thanks to our military and their families for their sacrifice on our behalf, especially those who suddenly find themselves in harm’s way.

Lee Riley

970-946-3856 (cell)

[email protected]

P.S. Remember, with my CRS referral network, I can provide you with a top notch Realtor anywhere in the country. CRS stands for Certified Residential Specialist, a professional designation that only 4% of the Realtors in the country have earned. If you or someone you know is relocating, I can refer you to a certified CRS agent.

GRI, CRS

2001 & 2014 Realtor of the Year

Phone (970) 731-4065

Fax (970) 731-4068

Cell (970) 946-3856

Email: [email protected]